No one likes disputes - certainly not when they are baseless, which sadly a large proportion of cardholder disputes are.

We try very hard to ensure that the merchant understands what remedies are available to them in fighting a chargeback/dispute that they believe should not exist.

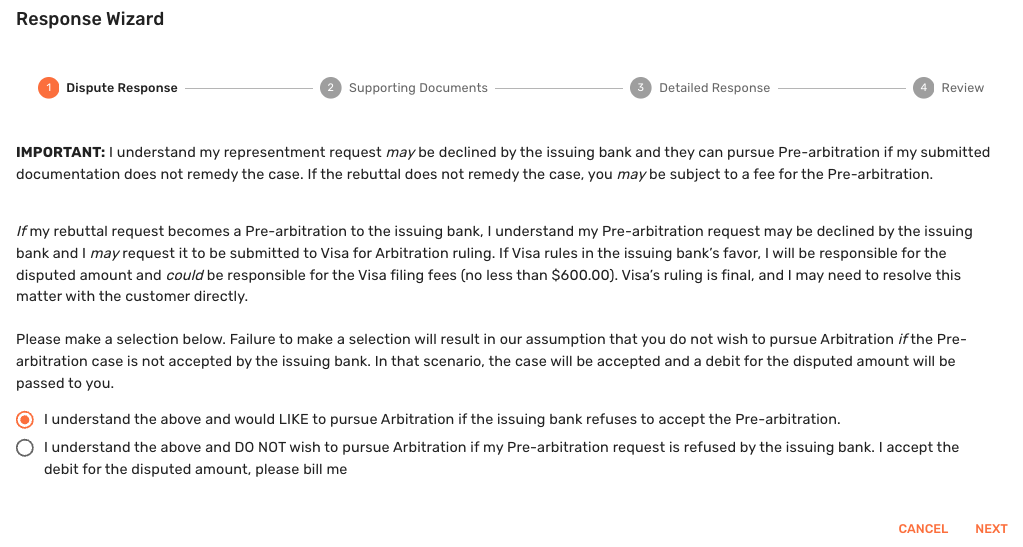

In your triceraportal.io chargeback engine, when you respond to a chargeback with documentation and to refute a cardholder claim, you are presented with an acknowledgement that looks like this:

In order to respond to the dispute, you have to accept this. To eliminate any confusion, let’s take it piece by piece and explain some things that are commonly overlooked in the heat of the moment.

Paragraph 1: The issuing bank can pursue pre-arbitration

IMPORTANT: I understand my representment request may be declined by the issuing bank and they can pursue Pre-arbitration if my submitted documentation does not remedy the case. If the rebuttal does not remedy the case, you may be subject to a fee for the Pre-arbitration.

As the processor, we have very little control over fee assessment or decisions when it comes to chargebacks. We make tools to help you respond, view the status of, and prevent chargebacks, but once they happen, it’s technically you (with us at your back) against the issuer & cardholder.

This paragraph simply states that the issuer may not accept your response. They (and the cardholder) may look at the evidence (or lack thereof) that you provided and side with the cardholder. They would, in this case, deny your rebuttal and you would have to choose what to do next.

Paragraph 2: Pre-Arbitration

If my rebuttal request becomes a Pre-arbitration to the issuing bank, I understand my Pre-arbitration request may be declined by the issuing bank and I may request it to be submitted to Visa for Arbitration ruling. If Visa rules in the issuing bank’s favor, I will be responsible for the disputed amount and could be responsible for the Visa filing fees (no less than $600.00). Visa’s ruling is final, and I may need to resolve this matter with the customer directly.

Note the words in bold italic font here. This is a warning message - aimed at making sure you know the process and what the worst case scenario is. This is not a statement informing you that responding to a chargeback costs $600.

To echo the explanation of Paragraph 1, the issuer may deny your rebuttal. They could loook at your evidence and decide you didn’t make a good case or they could have additional information from the cardholder in response to the evidence you submitted.

Pre-arbitration is the second fight after the merchant (you) has already fought the chargeback. It means the issuer or cardholder is refusing to accept the merchant’s evidence and is forcing the merchant to either concede, provide a stronger rebuttal, or risk the case moving to Visa arbitration. For a baseless chargeback, this is where the merchant must make the case airtight: not just “the customer is lying,” but “the issuer has failed to meet the Visa requirements for continuing this dispute after the merchant’s evidence.”

What is Pre-Arbitration?

From the merchant perspective, pre-arbitration is the last “do we settle this between the banks?” step before Visa is asked to make a final ruling. Arbitration only happens if the parties remain at odds after pre-arbitration.

How is Pre-Arbitration Different from Arbitration?

Pre-arbitration is not automatic arbitration. It is the step where the merchant/acquirer and issuer get one final chance to resolve the case. If the merchant accepts liability, it ends. If the merchant declines, the issuer may escalate to arbitration, but that is a separate next step.

The reason you have such a stern warning here is that if your pre-arb response is refuted it could automatically go to arbitration and we want you to know the risks.

Paragraph 3: Making a Choice

Please make a selection below. Failure to make a selection will result in our assumption that you do not wish to pursue Arbitration if the Pre-arbitration case is not accepted by the issuing bank. In that scenario, the case will be accepted and a debit for the disputed amount will be passed to you.

I understand the above and would LIKE to pursue Arbitration if the issuing bank refuses to accept the Pre-arbitration.

I understand the above and DO NOT wish to pursue Arbitration if my Pre-arbitration request is refused by the issuing bank. I accept the debit for the disputed amount, please bill me

As the unfortunate middle man in a scenario where roles and risks are not clearly defined or part of the normal everyday conversation for most merchants, we’re making it really clear what your intentions are so we can help you execute your intentions.

Option 1: I would like to pursue Arbitration

Again, it’s important to look at the bold italicized text. IF the issuing bank refuses to accept your response, with option 1 you are saying that you want to pursue Arbitration.

Option 2: I DO NOT wish to pursue Abitration

IF the issuing bank refuses to accept your response, with Option 2 you are basically saying if you don’t like what I have to offer here, there’s not much more I can do. This is common when you don’t have good evidence to support your claim.

Arbitration Fee: Who Pays?

The responsible party pays. If the merchant/acquirer wins, the issuer can be responsible. If the issuer wins, the acquirer/merchant side can be responsible. Visa can also split liability.

Rule of Thumb

When to Fight

Fight hard when the evidence is clean, the dollar amount is meaningful, and the case creates future risk. Take the loss when the economics, documentation, or card-brand risk make winning less valuable than ending it.

When to Take the Loss

When the evidence is emotional, not documented

The transaction is too small

Merchant terms are unclear

Merchant is in the wrong as well (procedural mistake, etc.)

Arbitration risk outweighs the recovery

Practical Decision Matrix

Situation | Recommendation |

|---|---|

High dollar + strong documents + customer clearly received benefit | Fight hard |

High dollar + weak documents | Fight, but cautiously; avoid arbitration unless improved evidence exists |

Low dollar + strong documents | Fight once, but probably do not escalate far |

Low dollar + weak documents | Take the loss |

Repeat friendly fraud/customer abuse | Fight harder than the dollar amount alone suggests |

Merchant policy was unclear or not accepted | Take the loss or settle |

Chargeback exposes a process gap | Take the loss, fix the process, prevent repeats |

Evidence directly disproves the cardholder’s claim | Fight hard |

Evidence only proves the merchant “believes” they are right | Take the loss or limit the fight |

Say it in Crayon

If you can prove the customer authorized it, received it, used it, accepted the terms, and was not owed a refund, fight. If you can only explain that the customer is wrong, but cannot prove it with documents, take the loss and tighten your process.

Always fight the first chargeback - respond with as much as you can muster.

Fight pre-arbitration only when evidence is strong,

Go near arbitration only wen the amount is meaningful, the documentation is excellent, and the merchant is comfortable with the risk.